Insurance companies love to claim that they have to charge customers more because they’re facing too many frivolous lawsuits or frivolous insurance claims. Don’t be fooled for a moment.

Insurance premiums in Texas are rising much faster than the payouts insurance companies are making to consumers, according to a report by the Texas Association of Consumer Lawyers. The group’s analysis of claims for hail-related property damage shows that losses incurred by insurance companies have stayed relatively flat, while premium revenues have steadily increased.

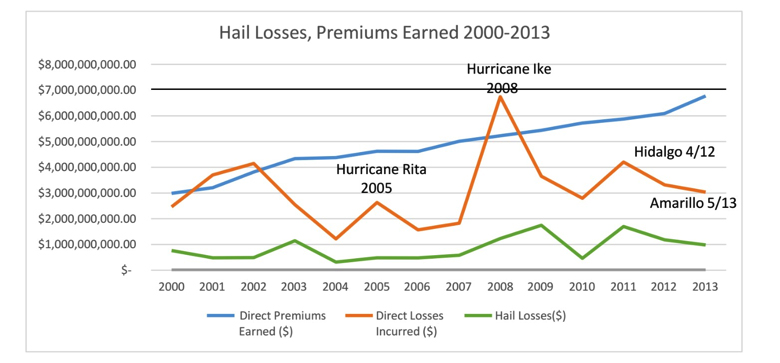

Between 2000 and 2013, the amount of money insurance companies collected in premiums nearly doubled from $2.99 billion to $6.77 billion. Over the same period, insurance companies’ overall losses—that is, the amount they have paid out in claims—have increased just 23 percent.

Hail-related losses, meanwhile, have seen only a 13 percent increase between 2000, when companies paid out $762 million, and 2013, when they paid $859 million. While payouts for hail claims have naturally fluctuated from year to year, they have remained relatively flat compared to the increases in premiums that Texans are being asked to pay.

Insurance company payouts as a percentage of premium revenues have stayed within a range that is associated with healthy profitability. (This metric, known as a loss ratio, does not include companies’ administrative costs and earnings on investments.) In 2012, Texas insurers paid a little more than half (54 percent) of their premiums out to cover losses. Anything below 60 percent is considered healthy for profitability, according to the Dallas Morning News. State Farm, in particular, hiked rates 20 percent that year, despite paying out just 47.5 percent of its premiums to customers to cover claims. In 2013, nearly all insurance companies in Texas hit the 60 percent loss ratio threshold, yet Allstate, Farmers and State Farm all announced rate hikes between 6 percent and 15 percent for many of their Texas customers. The year 2014 marked “a third straight year of healthy profits” for Texas’ biggest insurers, according to the Morning News.

Insurance company payouts as a percentage of premium revenues have stayed within a range that is associated with healthy profitability. (This metric, known as a loss ratio, does not include companies’ administrative costs and earnings on investments.) In 2012, Texas insurers paid a little more than half (54 percent) of their premiums out to cover losses. Anything below 60 percent is considered healthy for profitability, according to the Dallas Morning News. State Farm, in particular, hiked rates 20 percent that year, despite paying out just 47.5 percent of its premiums to customers to cover claims. In 2013, nearly all insurance companies in Texas hit the 60 percent loss ratio threshold, yet Allstate, Farmers and State Farm all announced rate hikes between 6 percent and 15 percent for many of their Texas customers. The year 2014 marked “a third straight year of healthy profits” for Texas’ biggest insurers, according to the Morning News.

To make matters worse, as insurance rates rise, insurers are offering less coverage to policyholders and are even seeking to limit lawsuits by homeowners. Insurance companies claim that they need to be protected from an increase in homeowner lawsuits, especially for damaged roofs from storms, even though we’ve just seen from the data that such lawsuits didn’t stop most insurers from posting healthy profits.

As of 2015, one-third of claims ended up in litigation in some parts of Texas, with policyholders alleging unfair practices or unpaid claims. Most of these lawsuits allege that Insurance companies have been overlooking and minimizing the costs of structural damage, roof damage, plumbing and electrical, wind and fire damage, water damage and more. The insurance companies are refusing to pay for all covered damages and doing out-come oriented investigations to push their agenda of making more profits at the cost of their homeowners they insure. They have developed a system of increasing premiums and underpaying claims to maximize profits.

There is no coincidence that insurance companies report record profits even in years where there have been several catastrophic claims in the United States. They have rigged the claims handling system to their favor and their benefit to underpay and under scope claims legitimate claims. They have routinely increased premiums across the board with no credible factual evidence to support their increases. We see insurance companies all over the television advertising their catchy commercials and slogans to lure insureds in to believing they will be protected if they are their customer. We can’t get away from their presence in most sporting events as well. They are able to do this because they are highly profitable and we must wonder were all those profits come from….we know the answer and so do you.